How the Fed’s Rate Decisions Actually Impact Your Mortgage — and What That Means for Orlando Homebuyers and Sellers

Let’s Talk About Everyone’s Favorite Mystery: Interest Rates

Hey, it’s Vinny with LIV ORL — and today we’re pulling back the curtain on one of the most confusing topics in real estate: how the Federal Reserve (the “Fed”) and its rate decisions actually impact your mortgage rate.

Because let’s be real — every time the news says, “The Fed raised rates again,” half the country panics, the other half shrugs, and most people have no clue what it really means for buying or selling a home in the greater Orlando area.

So, let’s make this simple, honest, and a little fun — because that’s how we roll here.

What the Fed Actually Controls (and What It Doesn’t)

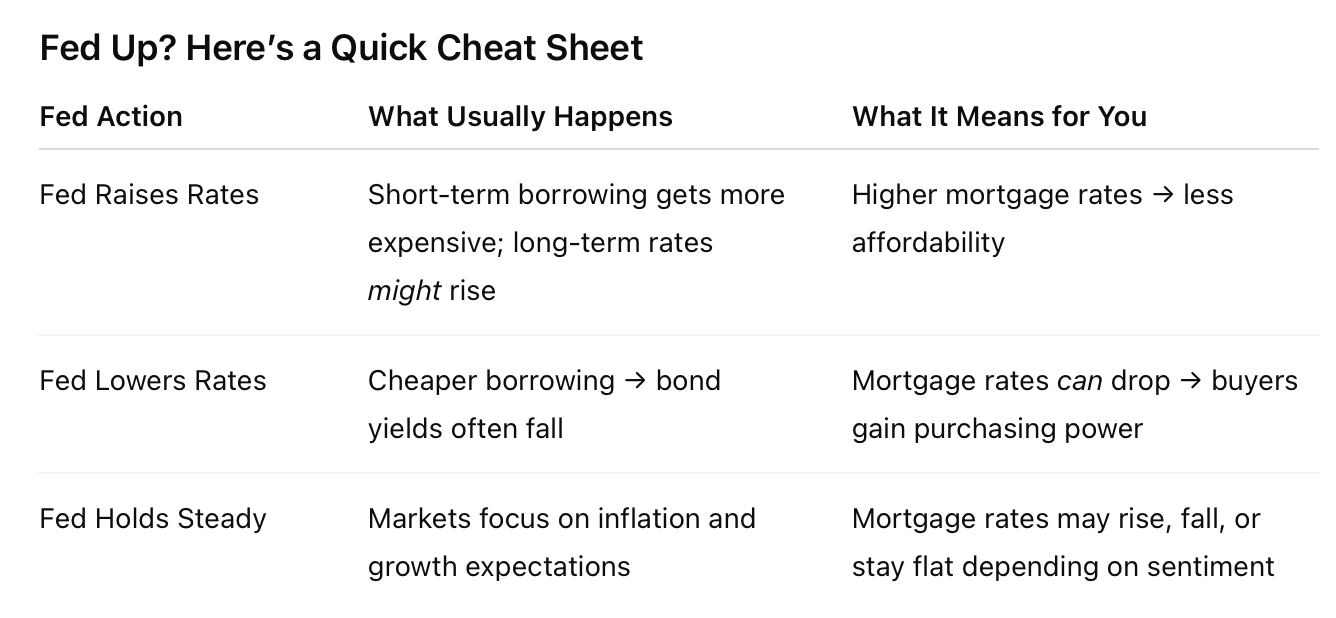

First things first — the Fed doesn’t directly control mortgage rates.

What it does set is called the federal funds rate, which is the rate banks charge each other to borrow money overnight.

When that rate goes up, short-term borrowing (like credit cards and car loans) usually gets more expensive. When it goes down, borrowing gets cheaper.

But your 30-year fixed mortgage? That’s a different animal. It’s more influenced by the bond market, specifically the yield on the 10-year U.S. Treasury.

Think of it like this:

The Fed fires the starting pistol at a race. The mortgage rate is the runner who takes off — but the runner’s speed depends on things like wind (inflation), terrain (economic outlook), and stamina (investor confidence).

How Fed Rate Changes Indirectly Affect Mortgage Rates

When the Fed raises its rate, it’s usually trying to cool off inflation — to slow down an overheated economy. That move sends signals through the financial world that can cause long-term bond yields (and mortgage rates) to rise.

On the flip side, when the Fed cuts rates, it’s trying to stimulate the economy. That often leads to lower yields on long-term bonds — which can lead to lower mortgage rates.

But here’s the kicker:

Mortgage rates don’t always follow the Fed’s lead right away.

If inflation stays stubborn or investors think the economy’s still running hot, mortgage rates might not drop even if the Fed cuts.

So, when you see a headline that says “Fed Cuts Rates — Mortgage Relief Ahead,” take it with a grain of salt. The markets have minds of their own.

Why This Matters So Much for Orlando’s Real Estate Market

Now, let’s bring it home — literally — to Orlando, Winter Garden, Windermere, Winter Park, and all our amazing Central Florida communities.

Interest rates shape how buyers and sellers behave, especially in the luxury market.

Here’s how:

1. Buying Power Shifts

A 1% change in mortgage rate can impact affordability by hundreds of thousands of dollars on a luxury property.

So when rates rise, some high-end buyers re-evaluate their price range. When rates fall, the market opens back up — and suddenly that dream home on Lake Butler or in Celebration doesn’t feel so far out of reach.

2. Sellers Stay or Go

When rates rise, homeowners with low-interest loans tend to stay put. (Who wants to give up a 3% rate for 7%?)

That means fewer listings and tighter inventory.

When rates drop, people feel freer to move — upgrading, downsizing, or relocating — which increases supply.

3. Buyer Psychology

In luxury real estate, psychology is everything.

When rates rise, buyers hesitate — they want to “wait and see.”

When rates fall or stabilize, confidence returns. That’s your moment to strike with a strong marketing strategy and a clear message.

What I’m Watching (So You Don’t Have To)

Here’s how I stay ahead for my clients and my team at LIV ORL:

-

The 10-Year Treasury Yield: It’s the closest cousin to the 30-year mortgage rate.

-

Inflation Data: If inflation cools, mortgage rates usually follow.

-

Fed Meeting Statements: The tone and language (“hawkish” vs “dovish”) can move markets fast.

-

Local Market Inventory: Rising rates can freeze sellers, so I monitor listing flow in places like Horizon West and Clermont.

I keep tabs on this stuff because it helps my clients make smart, timed moves — whether you’re buying your first home, upsizing, or listing a multi-million-dollar estate.

The Orlando Advantage (Even When Rates Rise)

Here’s the good news: Orlando is not an average market.

We’ve got population growth, job expansion, tourism, and investment appeal all working in our favor.

Even when national markets slow, Central Florida often keeps moving — because people still want to live here. Between the weather, no state income tax (maybe even no property tax soon...), and the lifestyle, our real estate market has built-in demand.

So while higher rates can cool things down temporarily, they don’t change the long-term fundamentals that make Orlando one of the strongest housing markets in the country.

Vinny’s Real-Talk Summary

-

The Fed sets short-term rates → mortgage rates respond indirectly based on inflation, bonds, and investor expectations.

-

Mortgage rates impact affordability, seller motivation, and buyer confidence.

-

In Orlando, the demand story is still strong — but timing the market right can make a major financial difference.

-

Stay informed, not panicked. Every rate shift brings new opportunity if you know how to play it.

Final Thoughts

The Fed might not know your name — but their decisions absolutely touch your wallet.

So the next time someone at brunch in Winter Park says, “The Fed’s raising rates again,” you can smile, sip your mimosa, and say:

“Yeah, but it’s the 10-year Treasury that’ll tell you where mortgage rates are really going.”

(Trust me — you’ll sound like the smartest person at the table.)